Annual Letter 23

Macro Overview, Portfolio and Lessons

Had a busy couple of months so posting with a slight delay.

The portfolio’s time-weighted return for the year was 32%, compared with 24% for the S&P500 index.

2023 Overview

2023 was an eventful year, to say the least.

Many started this year expecting a global recession, China to collapse, rates to stay higher for longer, the US defaulting on debt, and inflation to stick around. We also experienced auto workers and writers strikes.

With that much uncertainty, it wasn’t surprising that managers started the year the most bearish and overweight cash/bonds/defensive stocks since the periods after the crashes of 2008 and 2020.

While we can’t accurately predict macro events, what we can do is conservatively evaluate probabilities and determine how likely events might be, and how much they would affect individual stocks.

Researching these events and keeping a historical perspective, it soon became clear that markets were irrationally pessimistic.

Doom articles were coming out in droves:

The extreme bubble in stocks 'will end in tears' with the S&P 500 plunging 64%

When blood ran in the streets and many were calling for the end of markets, I was reminded of a quote by Howard Marks:

“There are three ingredients for success – aggressiveness, timing and skill – and if you have enough aggressiveness at the right time, you don’t need that much skill.”

When expectations are low, risk is lower, and potential returns are higher.

Thus, from the start of the year, I invested aggressively in undervalued cash-generative businesses residing in pockets where pessimism was highest.

I’ve made mistakes this year but being aggressive and only investing where there was a substantial margin of safety kept me outperforming.

Last year I wrote the following post arguing that the Fed will pause:

The Fed is Done: Beating the market by learning from the past

This post will cover why I believe the Federal Reserve is done raising interest rates, how money managers are positioned, and how we can gain an edge by learning from past cycles and searching for unpopular quality businesses in areas spurned by the market

Current Macro View

As the market starts pricing interest rate cuts and slowing QT, I mostly maintain the positioning detailed in the post above to profit from this change (emerging markets, biotech, small leveraged consumer discretionaries).

Higher rates have successfully brought Inflation below target while the consumer remained resilient.

As expectations for a lower US interest rate reduced the pressure on the Yuan, China started easing: lowering required reserves for banks (releasing hundreds of billions in capital), and lowering interest rates, ...

We are starting to see capital flowing to emerging markets as the cycle goes from US and Dollar outperformance to Emerging Markets.

Today most speculators are worried about the Middle East conflicts and supply chain disruption, the return of 70’s inflation, recession if the Fed overplays, and China's collapse.

The world is in a very different place today than in the 70s. There is a lower dependence on oil, the US today meets nearly all its energy needs from domestic production and the economy is much more globalized.

Regarding supply chains, the director of global macro research at Oxford Economics recently wrote: “Based on the IMF’s estimates, were container transport costs across all routes to remain around their current levels – about 90% higher than a month ago – this might boost inflation by around 0.6 percentage points in a year’s time, with the effects gradually subsiding thereafter” - probably inconsequential.

Regarding recession and the Fed cutting schedule, trying to predict this is futile. If Powel eases in time, the consumer will stay strong and we will profit.

If he drags the US to deflation and possibly a recession, I will profit from greater flows to emerging markets. Surprisingly, historically biotech is also a good recession hedge.

Major Positions Overview

CPS, STNE, and biotech were the major positive contributors to performance while BABA, and DLA were the main detractors.

I use a limited amount of derivatives to amplify the upside on some positions.

This is opinion not advice!

CPS

CPS is an auto parts supplier I invested in last year.

Chip shortages and supply chain issues in 2020-2021 hurt new car volumes, causing CPS to take on too much leverage amplifying poor performance in 2019 (china tariffs, increased competition abroad, and input cost inflation).

Revenues were declining, and they were bleeding cash causing markets to price bankruptcy as debt maturities came closer and it was unclear if management would be able to refinance at higher rates.

However, financial performance already started inflecting, they were focused on cost-cutting and efficiency, management was selling non-core assets ensuring they had enough liquidity to survive and insiders were buying shares in the public markets. They also had a strong competitive business moat in multiple products, and in turn, pricing power.

In December 2022 CPS managed to get into a backstop agreement to refinance its debt. While the price didn’t budge, I scrambled to gather more capital and liquidate minor positions, increasing my CPS position to a maximum size position.

As markets realized that the solvency risk was done, the stock rallied aggressively (almost tripling). A few months later, I came across Thomas Hayes of Great Hill Capital’s thesis about the ability of the business to generate 7$+ eps in a normalized environment and I am holding this for the earnings power as car volumes go up rather than a special situation.

In the past year, they have successfully negotiated contracts, returned to profitability, and are focusing on getting back to double-digit ROIC. As the average age of cars is still abnormally high (12.5+ yrs by S&P Global), demand is likely to keep rising.

STNE

StoneCo provides financial services to Brazillian businesses, focusing on small and medium-sized merchants.

The company started offering payment processing (as well as point of sale equipment) and moved on to offering financial services: prepayment of receivables, credit, banking and insurance, and software solutions such as ERP (resource and inventory planning), CRM (customer relations), and e-commerce.

The complete suite of payment, financial, and technology services combined with their focus on customer support with their hubs, makes churn low.

lays out the business and the differentiation well in their post:

From 2021 to 2023 the interest rate in Brazil was raised from 2% to 13.75%. As a financial services business, Stone’s business was temporarily impaired and it had to stop its credit business as the risk management was not prudent enough.

The stock price crashed 90%+ from all-time highs.

However, the business remained cash flow generative and kept growing the topline and clients fast, taking market share from competitors. The balance sheet is healthy and the new management is focusing on the right things and is guiding conservatively (and beating it). They are slowly rerolling credit but are doing this responsibly.

Also, the market Stone operates in Brazil is growing fast and capital is flowing back to Brazil.

I initiated a position at 9$ at the start of 23. While the stock doubled since, I still think it remains undervalued. As inflation drops in Brazil, rates are bound to go down and with them, StoneCo’s financial expenses.

Most investors don’t model lower interest rates improving Stone’s margin substantially and the potential of their banking and credit segments. When these events will pass, I might sell if the market gets buoyant but otherwise, I am perfectly content holding a growing high-quality business for the long term.

BABA

Quantitatively it is trivial that Baba is “cheap”. It is a high-quality fast-growing business trading at an Enterprise Value/FCF of about 5X. Baba has the same market cap as in the 2014 IPO while cashflows and revenues per share have grown massively.

The balance sheet is healthy (massive net cash position), insiders are scooping up shares, cash flow is high and growing, and management is focused on growth, ROIC, and buybacks.

Also, most of that cash flow comes from the China Commerce segment where they have an outstanding 40%+ market share.

This excludes:

the fast-growing International Commerce segment (AliExpress, Tryendol, …).

AliCloud with a 33%+ market share of the growing China cloud market. High-margin business as it matures

A third of Ant Group - owner of AliPay, processing more payment volume than Mastercard and Visa combined, have multiples of PayPal users…

Cainiao - Fast-growing logistics company worth billions

Many non-core investments such as 7.5% of XPENG.

However many say that China is Uninvestable.

If you opened a newspaper in the last 25 years they would have convinced you that China is on the verge of apocalypse.

1998. The Economist: China's economy entering a dangerous period of sluggish growth. (GDP +7.85%)

1999. Bank of Canada: Likelihood of a hard landing for the Chinese economy. (GDP +7.66%)

2000. Chicago Tribune: China currency move nails hard landing risk coffin. (GDP +8.49%)

2001. Wilbanks, Smith & Thomas: A hard landing in China. (GDP +8.34%)

2002. Westchester University: China Anxiously Seeks a Soft Economic Landing (GDP +9.13%)

2003. New York Times: Banking crisis imperils China (GDP +10.04%)

2004. The Economist: The great fall of China? (GDP +10.11%)

2005. Nouriel Roubini: The Risk of a Hard Landing in China (GDP +11.39%)

2006. International Economy: Can China Achieve a Soft Landing? (GDP +12.72%)

2007. TIME: Is China's Economy Overheating? Can China avoid a hard landing? (GDP +14.23%)

2008. Forbes: Hard Landing In China? (GDP +9.65%)

2009. Fortune: China's hard landing. China must find a way to recover. (GDP +9.40%)

2010: Nouriel Roubini: Hard landing coming in China. (GDP +10.64%)

2011: Business Insider: A Chinese Hard Landing May Be Closer Than You Think (GDP +9.55%)

2012: American Interest: Dismal Economic News from China: A Hard Landing (GDP +7.85%)

2013: Zero Hedge: A Hard Landing In China (GDP +7.77%)

2014. CNBC: A hard landing in China. (GDP +7.43%)

2015. Forbes: Congratulations, You Got Yourself A Chinese Hard Landing. (GDP +7.04%)

2016. The Economist: Hard landing looms for China (GDP +6.85%)

2017. National Interest: Is China's Economy Going To Crash? (GDP +6.95%)

2018. CNN: Forget the trade war, China's economy has other big problems. (GDP +6.75%)

2019. New York Times: China's Economy, by the numbers, Is Worse than it Looks (GDP +5.95%)

2020. WSJ: As Its Economy Slows, China Embraces a Weaker Currency (GDP +2.24%)

2021. Global Economics: Has China's Downfall Started? (GDP +8.45%)

2022. BBC: Five Reasons why China's Economy is in Trouble (GDP +2.99%)

2023. WSJ: A Financial Crisis in China Is No Longer Unthinkable (GDP +5.2%)

It is not surprising then, that short China is the second most crowded trade by BofA.

To put things in perspective, China grew its GDP 17X in these years.

A lot can be said about China’s demographics, real estate bubble, regional credit crisis, VIE structure, deflation, Taiwan, regulation, and a myriad of other issues.

However, most of these risks are not new and have a limited effect on Baba's domestic and international operations. As the business is of the highest quality, and management is investing aggressively in growth, I feel comfortable waiting for the price to catch up as fundamentals are improving.

Management is focused on unlocking shareholder value by issuing dividends, buybacks, pursuing spin-offs, or selling off non-core businesses and insiders are buying record amounts of (undervalued) stock in the public market.

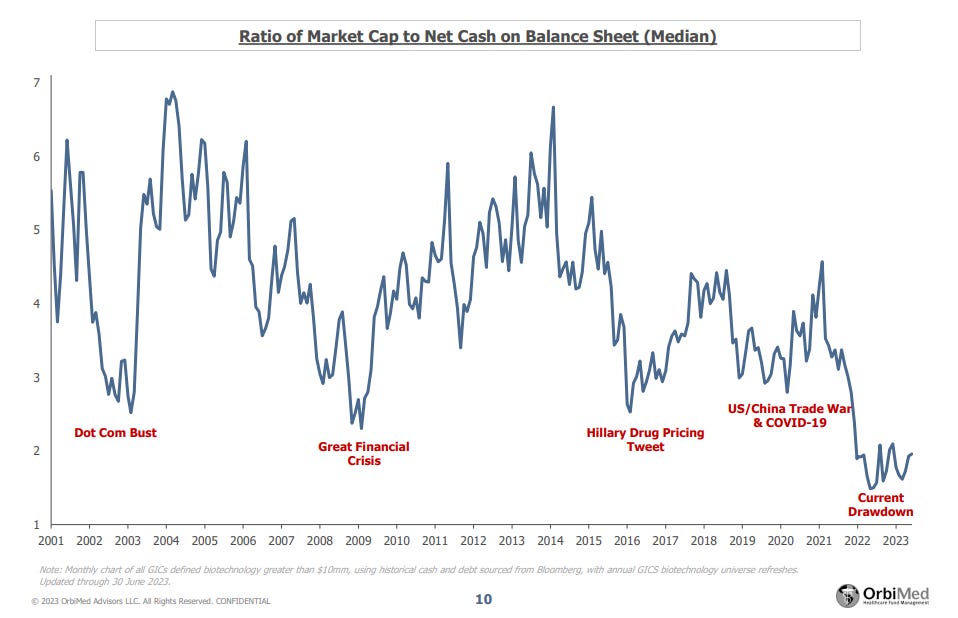

XBI

Was a positive contributor in 23 and I expect it to keep outperforming. I explained the rationale in the post in Oct but generally biotech valuations are the lowest they have been since before huge rallies. Biotech companies (especially small ones) will benefit from rate reductions as they require capital and M&A.

The Idea here is that buying indexes of growing companies at historically low valuations usually turns out great.

DLA

Detracted from performance in 2024 as I got in a tad early. I expect this to start outperforming in the second half as they return to normal input costs and production and the market starts pricing their assets and growing segments.

ASOS

A smaller 3.5% position to get some UK exposure. Hurt by inflation and rates, extremely high operating leverage. Overrated solvency risk as they refinanced debt returned to positive cash flow and have supportive powerful insiders.

Insiders rejected offers to buy the business for 3X the market cap and are buying a ton of stock.

GCI

The owner of USA Today and other regional publications.

A smaller 2% position, is generally a debt reduction story with the optionality of cost cuts, a huge reader base to monetize, a digital transformation, and possible lawsuit proceeds against Google.

With high consistent FCF and a heavy debt burden, management is focused on selling assets and buying discounted debt, reducing their interest expense and thus, growing their cash flow (allowing more debt repayment).

Paypal

Smaller 3% position. Investors fail to understand Braintree and the benefit to merchants, the new CEO focuses on profitable growth, they have a high cashflow yield, and buyback a lot of shares.

They are also a bit of an inflation hedge as they profit from transaction volumes (that go up with inflation).

Acquisitions and possible use of data to enhance the buying experience (the CEO talked about it in the last call) add nice optionality.

Lessons from 2023

If I had to sum up my experience in 2023 it would be these 3 lessons:

High Turnover

Until the fourth quarter of the year, I had small 1-2% asymmetric trades in securities where the quality of the business and/or conviction was not high enough for me to put considerable capital.

While the IRR of these positions was satisfactory, the need to stay on top of these caused unneeded stress and ultimately distracted me from what mattered.

Margin Of Safety

“Luck is what happens when preparation meets opportunity” ~Seneca

I had a few positions this year where I either failed to understand important facets of the investment (Didn’t model interest rate change correctly in DLA and Stne, …) when buying or unknowable macro events (UAW strike for CPS).

With both, I was lucky. The positions were entered at such a discount to intrinsic value (margin of safety) that big mistakes were not fatal.

The Importance Of Quality

In the book, The Intelligent Investor, the father of value investing Benjamin Graham teaches us that the investor engages in pricing while the speculator tries his luck in timing.

Pricing means buying businesses below value and selling them when the price gets ahead of fundamentals. Something I learned this year to think about is that intrinsic value is not static.

A high-quality business with a high return on invested capital improves while you wait for the price while low-quality businesses destroy value over time.

Thus, with low-quality businesses, we engage in timing even when we buy “right” as we gamble that the value is realized before it dissolves.

Some positions will take time to rally. As long as the business has a return on invested capital at a rate I find satisfying, and management respects shareholders, I am content waiting.

Book Recommendation

Loved reading Margin of Safety by Seth Klarman, and The Dhando Investor by Mohnish Pabrai.

Currently reading Security Analysis 7th edition and Financial Shenanigans and enjoying both.

Video Recommendation

Came by this beginner lecture by Bill Ackman and been recommending it to friends since. His ability to explain simply and comprehensively is admirable.

Companies on my radar:

Currently looking at Nabors and Leat.

Disclaimer: Nothing in the post constitutes financial advice. Consult your financial advisor.

Congratulations on the year! Great letter and thank you for the shoutout.